33 percent rent increases and bidding wars on rentals are the new norm in some parts of America as reopening comes with big price hikes.

Lauren Campos opened the door to her Phoenix apartment last week to find a note stuck in the door frame. Her rent was going up nearly $400 a month, the note said,a 33 percent increase.

Campos and her fiancee read the letter in shock. The property management company gave them four days to decide whether to commit to stay or leave by the end of July. They spent the rest of the day poring over apartment listings online, only to realize they would either have to move or downsize from their two-bedroom place to a one-bedroom.

“It almost feels like there is nowhere to go. It’s just insane everywhere,” said Campos, 28, a lifelong Phoenix resident who has noticed a growing number of California license plates in her complex’s parking lot. “It feels like I’m being chased out of my own home, and it’s the worst feeling in the world.”

Rents are starting to surge in many parts of the country as the economy reopens and young people return rapidly to cities. On top of the influx of millennials and Gen Z renters coming back after staying with family or friends, people who can work from anywhere are still relocating to lower-cost cities, and the hot home sale market has caused some baby boomers to sell their family homes and rent again now that their kids are grown.

Nationwide, rent prices are up 7.5 percent so far this year, three times higher than normal, according to data from Apartments.com. Analysts expect rent prices to keep climbing for the foreseeable future, a major burden for renters and a warning sign that higher inflation could linger far longer than the White House and Federal Reserve keep predicting.

“I think we’re going to see increases for the next 12 to 18 months,” said Robert Pinnegar, president of the National Apartment Association. “We’ve never had three generations in the rental housing space, at least not in the numbers we’re seeing now.”

Demand for two particular types of rentals is especially high: single-family homes and apartments in smaller citiesthat have less inventory. Rents for single-family homes are growing at the fastest pace in 15 years, according to data firm CoreLogic. Parts of the country that used to be considered affordable are suddenly experiencing the kind of rent frenzy with bidding wars and surging prices thathad previously been exclusive to mega cities like San Francisco and New York City.

“I tell my buyers: It’s a terrible time to buy, but it’s an even worse time to rent,” said Chey Tor, a Realtor at Re/Max Ascend Realty in Scottsdale, Ariz.

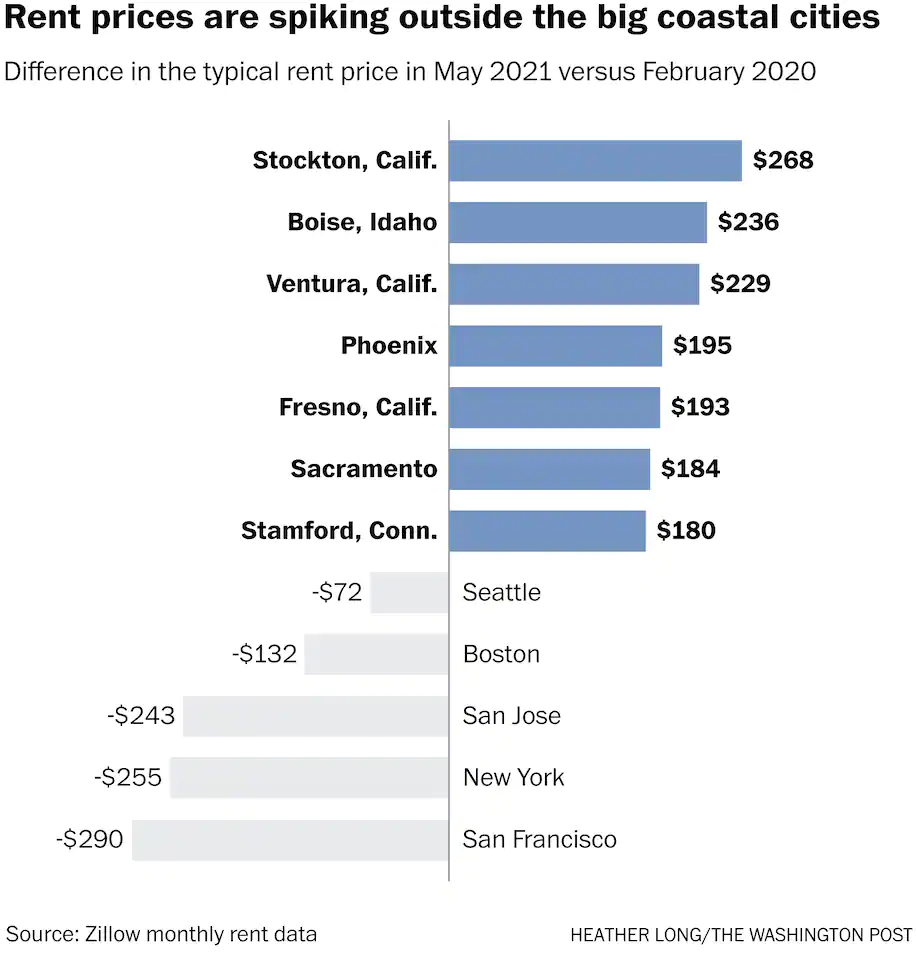

Phoenix is among more than a dozen cities that have seen over a 10 percent spike in rents in the past year, according to Zillow, a real estate website for sales and rentals. The top cities for soaring rents include Boise, Idaho, Riverside, Calif., Spokane, Wash., Tucson, Stockton, Calif., and Las Vegas — what Realtors have dubbed the “Inland West.” Realtors in these places say they have been inundated with calls from young people and families who want to relocate from pricier parts of California and Washington state.

San Francisco and New York City are among only a handful of cities where the typical rent price is still below pre-pandemic levels, according to Zillow, though there are signs of a rebound there, too. So-called “rent concessions” where landlords offer a month or two of free rent or waive the deposit have dropped sharply in recent weeks. In November, 60 percent of downtown urban listings on Apartments.com offered concessions. In June, just 35 percent did.

Jason Geroux, owner of 4:10 Real Estate in Phoenix, said he has managed rentals for nearly 15 years and never seen anything like this. His rental listings are often getting more than a dozen applications. People call him and offer to pay more than the asking price for the rental, effectively creating bidding wars on rental properties. On two recent listings, so many people offered to pay more money that he had all the applicants write down their best offer.

“Potential renters are saying, ‘Hey, what if I offer $500 more a month?’ It’s just crazy stuff,” Geroux said. “For past 12 months we’ve seen supply going down and demand going up. It’s just caused things we haven’t seen before.”

Landlords in many of these inland cities are realizing the power they suddenly have. One of Geroux’s clients recently asked for a 50 percent rent increase. Geroux, an advocate for affordable housing, tried to talk the client to a lower amount, but he was not successful. Many cities outside the coasts do not have caps on how much rent prices can go up because they have never seen this kind of surge before.

If a renter is not willing to pay the higher rate, landlords are confident they can find someone else — or sell the property.

Nick Kasoff, a landlord of 15 properties in Ferguson, Mo., gets at least a call a day from investors asking if he is willing to sell one of his rental homes. So far, he has said no.

“I can’t even answer my phone anymore,” Kasoff said. “As soon as they ask for Nicholas, I know exactly what it is. No one calls me Nicholas unless they look me up on property tax records.”

For years, the United States has not had enough rental properties, especially affordable ones in urban areas. The problem is even more acute now as some building projects were put on hold during the pandemic and some rental homes were sold off this spring during the housing market boom.

Michael Kobold has been renting in Boise since he lost his home in the financial crisis of 2008-2009. A year ago, he was paying $750 to rent a house with a big garage for his art studio. The rent jumped to $1,450 this month. Kobold felt he had no choice but to pay it. He brought in another roommate to help split costs, but even with three of them now, money is tighter than it was before.

“If you leave, then you’ll end up out on the street,” said Kobold, who is 69. “The problem is all these people from California moving in here. They are paying for a house sight unseen.”

The trend of small and midsize cities seeing surging rents is different from in the past. According to Zillow, the last time rent increases nationwide were jumping this much was 2015 when San Francisco and San Jose topped the list of highest rent increases along with Denver, Honolulu and Portland, Ore. So far in 2021, none of those cities appear in the top 80 for rent increases, according to Zillow data through May.

The pandemic caused Americans to put a greater emphasis on wanting more space and a more reasonable cost of living. But as prices rise in smaller cities, especially in the Inland West and Sun Belt, economists and Realtors warn there will be unforeseen consequences, and it could take years before enough housing is built in these areas to alleviate price pressures.

“It’s hard to keep up with the demand shift in the housing market because building homes is slow and encumbered by a lot of red tape and geographic challenges,” Zillow chief economist Jeff Tucker said.

Wall Street is also starting to notice the high demand and low supply in the rental market and the potential profits that could be made. Private equity firm Blackstone recently purchased Home Partners of America, which manages about 17,000 rental homes, for $6 billion. And J.P. Morgan Asset Management and American Homes 4 Rent announced a deal last year to build more rental homes, targeting the West and Southeast.

It is not clear yet what all of these trends will mean, but most economists and investors predict high demand for rentals for months to come. That is likely to push up inflation since rent makes up about 40 percent of the consumer price index that the U.S. government calculates each month.

The latest inflation data from May showed a modest 1.8 percent increase in rents for main residences, but experts think that could rise this summer and fall, especially given what they are seeing from sites like Apartments.com and Zillow. The fact that wages are rising at one of the fastest paces since the early 1980s also gives landlords confidence to hike rents.

“Core inflation could stick over 2 percent faster and longer in this expansion because shelter inflation should pick up,” said Logan Mohtashami, a former mortgage broker who is now lead analyst for HousingWire. “If we do really see wage growth at the bottom end, landlords will ask for more rent.”

In many parts of the country that have not seen this kind of rent pressure before, it is hitting especially hard — and making people worry that prices will keep climbing. The United States also has a growing number of people living on fixed incomes as they retire, making them especially hard hit by rent increases.

Pamela Porter, 68, lives in a one-bedroom apartment in a retirement community in Fort Worth. She just received notice her rent is rising by $40 a month to $780 — a 5 percent hike.

“I’ve noticed food prices going up. And gasoline. Oh my. That shot through the roof,” Porter said. She said $40 may not sound like a lot, but “that increase could definitely impact my ability to buy groceries and buy my medicine. I’m not going to even mention car repairs. Life shouldn’t be this hard.”